The Quadrant Deep-Dive

The data reveals a stark reality: the middle is a dangerous place to be, as the retail banking sector undergoes a profound stratification.

Why some banks are converting cultural relevance into real market differentiation while others risk becoming invisible commodities in the financial lives of modern consumers

Chase and Capital One have cracked the code, proving that high market energy and elite cultural fluency are the ultimate competitive moat.

In an era of commoditized banking, momentum is the only thing keeping legacy giants like U.S. Bank, PNC Bank, and TD Bank from fading in a noisy and competitive market

Digital disruptors like SoFi and Rocket Mortgage might have the “cool factor,” but without deeper cultural relevance, their growth trajectory is a house of cards.

Analysis methodology: Cultural Fluency & Momentum are both measured on a scale of 0-100 based on survey responses from >4500 18+ U.S. consumers. Both measures are predictive of purchase intent & brand favorability, key leading indicators of sustained sales leadership. Cultural Fluency is measured using B-CFQ, a proprietary Collage Group score based on Fit, Relevance, Trust, Values, Memories & Advocacy. Momentum is a measure of whether a brand is gaining or losing traction in the market. Brands included in this chart met a minimum brand awareness threshold of 65%.

Banking isn’t just about ledger lines anymore, it’s about lifestyle alignment. The current landscape is a battlefield where traditional titans are desperately trying to learn the language of the modern consumer, while nimble fintechs are realizing that “disruption” doesn’t automatically equal cultural fluency. We’re seeing a massive shift where the “cool factor” (a.k.a momentum) is being tested against trust and resonance (a.k.a Brand Cultural Fluency).

The industry’s health is no longer measured by assets under management alone, but by how effectively a brand can insert itself into the cultural conversation. Brands that are rising are capturing the imagination of a younger and more diverse public, but only those with high Brand Cultural Fluency (B-CFQ) scores are actually sticking the landing. It’s a game of high stakes where being steady is just a slow way of falling behind.

The data reveals a stark reality: the middle is a dangerous place to be, as the retail banking sector undergoes a profound stratification.

Leading Brands like Chase (B-CFQ: 71; Momentum: 41%) and Capital One (B-CFQ: 68; Momentum: 38%) are firing on all cylinders by successfully merging high-velocity market energy with a sophisticated understanding of diverse consumer segments.

These dominant players have separated themselves from the pack, maintaining both the highest cultural resonance and the strongest perception of growth in the industry.

Trailing Brands are struggling to get a foothold in consumer’s minds and wallets. TD Bank (B-CFQ: 51; Momentum: 20%) represents a cluster that is falling behind in both perception and cultural relevance.

The industry’s health is essentially polarized, while top performers reach new heights of market energy, these struggling institutions remain stuck in a low-resonance loop that risks permanent irrelevance.

Meanwhile, a large group of brands in the Middle of the Pack, including Wells Fargo (Momentum: 31%) and Rocket Mortgage (Momentum: 31%), are essentially treading water; they possess enough market energy to stay visible but lack the elite B-CFQ scores required to challenge the industry leaders.

This division suggests that merely maintaining a steady trajectory is no longer enough to survive, as the gap between those who own the cultural conversation and those who are excluded from it continues to widen. The segment-level data shows that the divide is even sharper when viewed through specific cultural and generational audiences.

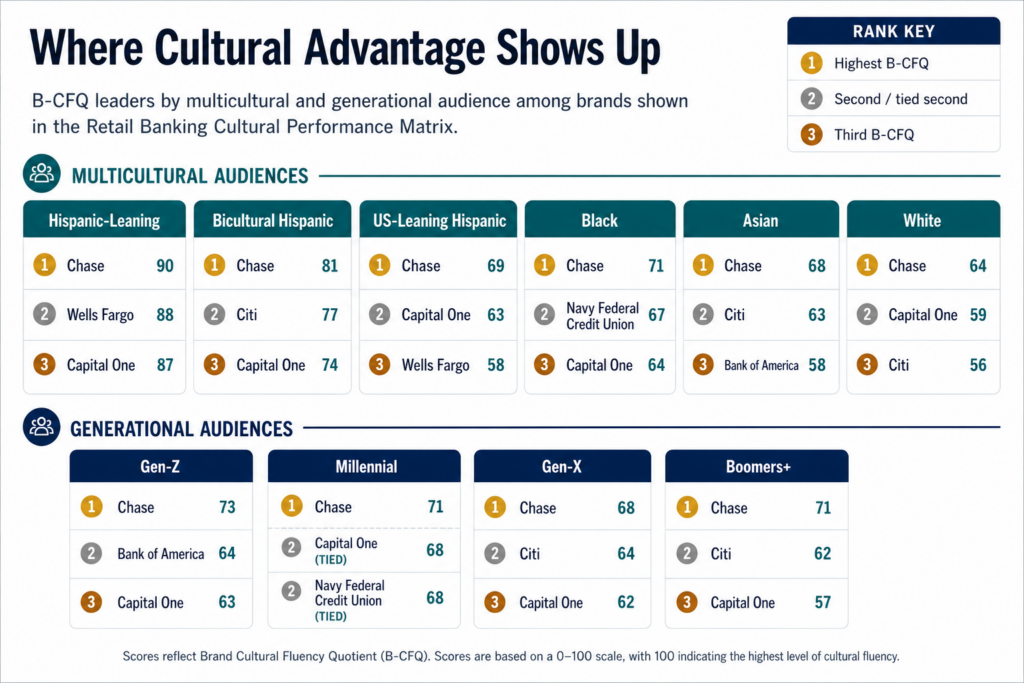

The matrix tells us who is winning overall, but the cultural audience cuts reveal where those advantages are strongest. Across the brands that met the chart’s awareness threshold, Chase is the clearest universal leader: it ranks first in B-CFQ across every multicultural group and every generation measured.

Multicultural Leaders: Chase leads Heritage-Leaning Hispanic consumers with a B-CFQ score of 90, Bicultural Hispanic consumers at 81, Black consumers at 71, Asian consumers at 68, US-Leaning Hispanic consumers at 69, and White consumers at 64. That consistency matters because it suggests Chase’s cultural advantage is not dependent on one audience segment carrying the average.

The challenger set changes by audience: Wells Fargo is especially strong with Heritage-Leaning Hispanic consumers, where it scores 88 and sits just behind Chase. Citi has a sharper cultural story than the topline matrix alone suggests, ranking second among Bicultural Hispanic consumers at 77 and Asian consumers at 63. Navy Federal Credit Union also breaks through with Black consumers, ranking second with a score of 67.

Generational Leaders: Chase also leads every generation, with scores of 73 among Gen-Z, 71 among Millennials, 68 among Gen-X, and 71 among Boomers+. But the next-best brands vary in telling ways: Bank of America moves into the #2 position among Gen-Z with a score of 64, Capital One is strongest among Millennials at 68, and Citi rises to #2 among Gen-X and Boomers+.

The strategic implication is clear: broad cultural fluency creates the strongest foundation, but segment-specific strengths can reveal hidden paths to momentum. For brands outside the lead quadrant, the fastest route forward may not be trying to win everyone at once, but identifying the audiences where they already have permission to matter and building from there.

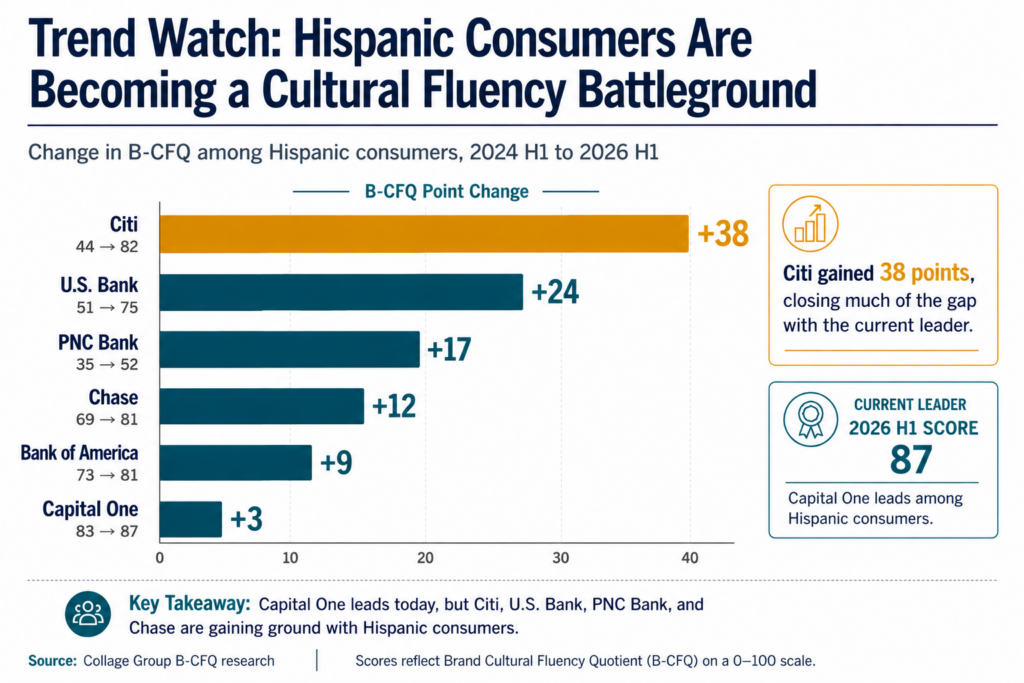

Looking at B-CFQ performance over time, an interesting story emerges. The matrix shows who is winning today, but the trendline over a two-year horizon (2024 H1 to 2026 H1) shows which brands are gaining cultural ground fastest. On that view, Hispanic consumers stand out as one of the clearest movement stories in retail banking.

While Capital One holds the highest current B-CFQ score among Hispanic consumers at 87, the brands chasing it are gaining ground quickly. Citi has seen the biggest improvement with Hispanic consumers over two years, surging from 44 to 82, a +38 point gain. U.S. Bank has also made major leaps, rising from 51 to 75, while PNC Bank climbed from 35 to 52, over a two-year window. Chase, already one of the strongest cultural performers in the category, continues to build on its advantage, moving from 69 to 81 over two years.

This matters because Hispanic consumers are one of the largest and fastest-growing segments in banking. For retail banks, winning this cultural audience is no longer a niche growth opportunity, but central to long-term market share growth.

| For Leading Brands (Chase, Capital One) | These brands are the current MVPs. Their momentum is the envy of the industry. The goal now is to guard that B-CFQ like a vault; don’t let corporate stiffness dilute the cultural fluency that’s driving your growth. |

| For the Middle of the Pack with stronger Cultural Fluency (Bank of America, Wells Fargo, Citi) | These brands are reliable classics, but they’re also at risk of losing their edge. While B-CFQ scores are solid, these brands need a shot of adrenaline. To kick start their growth trajectory, they need to stop acting like a utility and start acting like a cultural catalyst. |

| For the Middle of the Pack with stronger Momentum (SoFi, Rocket Mortgage) | They’ve got the flash, but do they have the substance? For example, SoFi’s momentum (32%) is high, but their B-CFQ (44) suggests a “one-hit wonder” in the cultural charts. They’ll need to turn that high energy into deep consumer resonance before the hype fades. |

| For Trailing Brands and those on the Edge (PNC, SoFi, U.S. Bank, TD Bank) | While several of these brands are aiming for specific regions and audiences, it may be time for a refresh. Lower momentum scores means these brands could be falling behind, or worse. The good news is that trailing doesn’t need to be permanent and brands in this quadrant can seize their unique opportunities to tackle the first available inroads to increasing either Cultural Fluency or momentum. |

If you want to dive deeper into the specific cultural factors separating Retail Banking leaders fill out the form to schedule a 20-minute consultation with our cultural strategists.

The Cultural Performance Matrix™ is anchored in Collage’s proprietary Brand Cultural Fluency Quotient (B-CFQ), which measures how effectively a brand connects across diverse consumer segments – based on drivers like fit, relevance, trust, values, memories, and advocacy. Combined with market momentum – an indicator of whether a brand is gaining or losing traction – the framework provides a dynamic view of performance, helping brands understand not just how they are perceived, but how that perception translates into real-world traction. Brands that improve their ranking on the Matrix consistently see gains in favorability and purchase intent.

This particular study is based on survey data from 4,500 U.S. consumers.